SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM 10-K

|

| | |

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For The Fiscal Year Ended July 2, 2011 |

| | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No. 1-15583

DELTA APPAREL, INC.

(Exact name of registrant as specified in its charter)

|

| | |

Georgia (State or other jurisdiction of incorporation or organization) | | 58-2508794 (I.R.S. Employer Identification No.) |

322 South Main Street

Greenville, SC 29601

(Address of principal executive offices) (zip code)

Registrant’s telephone number, including area code: (864) 232-5200

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

Title of Each Class | | Name of Each Exchange on Which Registered |

Common Stock, par value $0.01 | | NYSE Amex |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned filer, as defined in Rule 405 of the Securities Act. Yes o No þ.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | |

Large accelerated filer o | | Accelerated filer þ | | Non-accelerated filer o | | Smaller reporting company o |

| | | | (Do not check if a smaller reporting company) | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ.

As of January 1, 2011, the aggregate market share of the registrant’s voting stock held by non-affiliates of the registrant (based on the last sale price for such shares as quoted by the NYSE Amex) was approximately $96.0 million.

The number of outstanding shares of the registrant’s Common Stock as of August 22, 2011 was 8,388,413.

DOCUMENTS INCORPORATED BY REFERENCE:

Certain information required in Part III of this Form 10-K shall be incorporated from the registrant’s definitive Proxy Statement to be filed pursuant to Regulation 14A for the registrant’s 2011 Annual Meeting of Shareholders currently scheduled to be held on November 10, 2011.

TABLE OF CONTENTS

|

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

EX-21 | |

EX-23.1 | |

EX-31.1 | |

EX-31.2 | |

EX-32.1 | |

EX-32.2 | |

Cautionary Note Regarding Forward Looking Statements

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements made by or on behalf of the Company. We may from time to time make written or oral statements that are “forward-looking,” including statements contained in this report and other filings with the Securities and Exchange Commission (the “SEC”), in our press releases, in oral statements, and in other reports to our shareholders. All statements, other than statements of historical fact, which address activities, events or developments that we expect or anticipate will or may occur in the future are forward-looking statements. The words “estimate”, “project”, “forecast”, “anticipate”, “expect”, “intend”, “believe” and similar expressions, and discussions of strategy or intentions, are intended to identify forward-looking statements.

The forward-looking statements in this Annual Report are based on our expectations and are necessarily dependent upon assumptions, estimates and data that we believe are reasonable and accurate but may be incorrect, incomplete or imprecise. Forward-looking statements are also subject to a number of business risks and uncertainties, any of which could cause actual results to differ materially from those set forth in or implied by the forward-looking statements. The risks and uncertainties include, among others:

| |

• | the volatility and uncertainty of cotton, other raw materials, transportation and energy prices; |

| |

• | the general U.S. and international economic conditions; |

| |

• | changes in consumer confidence, discretionary consumer spending and demand for apparel products; |

| |

• | the financial difficulties encountered by our customers and credit risk exposure; |

| |

• | the competitive conditions in the apparel and textile industries; |

| |

• | changes in environmental, tax, trade, employment and other laws and regulations; |

| |

• | any significant litigation in either domestic or international jurisdictions; |

| |

• | changes in the economic, political and social stability at our offshore locations; |

| |

• | the relative strength of the United States dollar as against other currencies; |

| |

• | any restrictions to our ability to borrow capital or obtain financing; |

| |

• | the ability to grow, achieve synergies and realize the expected profitability of recent acquisitions; |

| |

• | the impairment of acquired intangible assets; |

| |

• | changes in our information systems related to our business operations; |

| |

• | any significant interruptions with our distribution network; |

| |

• | the ability of our brands and products to meet consumer preferences within the prevailing retail environment; |

| |

• | the ability to obtain and renew our significant license agreements; |

| |

• | implementation of cost reduction strategies; |

| |

• | any negative publicity regarding domestic or international business practices; and |

| |

• | the illiquidity of our shares and volatility of the stock market. |

A detailed discussion of significant risk factors that have the potential to cause actual results to differ materially from our expectations is described in Part 1 under the heading of “Risk Factors.” Accordingly, any forward-looking statements do not purport to be predictions of future events or circumstances and may not be realized. We do not undertake publicly to update or revise the forward-looking statements even if it becomes clear that any projected results will not be realized.

PART I

“Delta Apparel”, the “Company”, “we”, “us” and “our” are used interchangeably to refer to Delta Apparel, Inc. together with our domestic wholly-owned subsidiaries, including M.J. Soffe, LLC (“Soffe”), Junkfood Clothing Company (“Junkfood”), TCX, LLC ("TCX"), To The Game, LLC (“To The Game”), Art Gun, LLC (“Art Gun”), and other international subsidiaries, as appropriate to the context.

We were incorporated in Georgia in 1999 and our headquarters is located at 322 South Main Street, Greenville, South Carolina 29601 (telephone number: 864-232-5200). Our common stock trades on the NYSE Amex under the symbol “DLA”.

We operate on a 52-53 week fiscal year ending on the Saturday closest to June 30. The 2011 fiscal year was a 52-week year and

ended on July 2, 2011. The 2010 fiscal year was a 53-week year and ended on July 3, 2010. The 2009 fiscal year was a 52-week year and ended on June 27, 2009.

OVERVIEW

Delta Apparel, Inc. is an international design, marketing, manufacturing and sourcing company that features a diverse portfolio of lifestyle branded activewear apparel and headwear and high-quality private label programs. We specialize in selling casual and athletic products through a variety of distribution channels. Our products are sold across distribution tiers and in most store types, including specialty stores, boutiques, department stores, mid-tier and mass channels. From a niche distribution standpoint, we also have strong distribution at college bookstores and the U.S. military. Our products are made available direct-to-consumer on our websites at www.soffe.com, www.junkfoodclothing.com, www.saltlife.com and www.deltaapparel.com. Additional products can be viewed at www.2thegame.com and www.thecottonexchange.com. We believe this diversified distribution allows us to capitalize on our strengths to provide casual activewear and headwear to consumers purchasing from most types of retailers.

We design and internally manufacture the majority of our products, which allows us to offer a high degree of consistency and quality controls as well as leverage scale efficiencies. One of our strengths is the speed in which we can reach the market from design to delivery. We have manufacturing operations located in the United States, El Salvador, Honduras and Mexico, and use domestic and foreign contractors as additional sources of production. Our distribution facilities are strategically located throughout the United States to better serve our customers with same-day shipping on our catalog products and weekly replenishments for retailers.

ACQUISITIONS

We have become a diversified branded apparel company through the seven acquisitions we have completed since October 2003. These acquisitions have added well-recognized brands and licensed properties to our portfolio, expanded our product offerings and broadened our distribution channels and customer base.

|

| | | | |

Business | | Date of Acquisition | | Business Segment |

The Cotton Exchange | | July 5, 2010 | | Branded |

Art Gun | | December 28, 2009 | | Branded |

To The Game | | March 29, 2009 | | Branded |

FunTees | | October 2, 2006 | | Basics |

Intensity Athletics | | October 3, 2005 | | Branded |

Junkfood Clothing | | August 22, 2005 | | Branded |

M.J. Soffe | | October 3, 2003 | | Branded |

The Cotton Exchange Acquisition

The Cotton Exchange designs and markets decorated casual apparel to college bookstores, the U.S. military and other retail accounts. On June 11, 2010, we formed a new North Carolina limited liability company, TCX, LLC, as a wholly-owned subsidiary of M.J. Soffe, LLC. Pursuant to an Asset Purchase Agreement dated July 5, 2010, on July 12, 2010, TCX acquired substantially all of the net assets of HPM Apparel, Inc. d/b/a The Cotton Exchange, including accounts receivable, inventory, and fixed assets, and assumed certain liabilities. The total purchase price, which included a post-closing working capital adjustment, was $9.9 million. We finalized the valuation for the assets acquired and liabilities assumed and have determined the final allocation of the purchase price. No goodwill or other intangible assets were recorded in conjunction with the acquisition of The Cotton Exchange.

The Cotton Exchange has a strong reputation selling USA made collegiate apparel to college bookstores under “The Cotton Exchange” brand. The Cotton Exchange was formed in 1984 and is recognized in the industry for the quality of its garments, graphic designs, and most importantly its service to customers. The Cotton Exchange is headquartered in Wendell, North Carolina and is operated as the bookstore division of Soffe within our branded segment.

BUSINESS SEGMENTS

We operate our business in two distinct segments: branded and basics. Although the two segments are similar in their production processes and regulatory environment, they are distinct in their economic characteristics, products and distribution methods.

The branded segment is comprised of our business units focused on specialized apparel garments and headwear to meet consumer preferences and fashion trends, and includes Soffe (which includes The Cotton Exchange as the bookstore division of Soffe), Junkfood, To The Game and Art Gun. These branded embellished and unembellished products are sold through specialty and boutique shops, upscale and traditional department stores, mid-tier retailers, sporting goods stores, college bookstores and the

U.S. military. Products in this segment are marketed under our primary brands of Soffe®, Intensity Athletics®, The Cotton Exchange®, Junk Food®, The Game®, Salt Life® and Realtree Outfitters® as well as other labels. The results of The Cotton Exchange, Art Gun and To The Game have been included in the branded segment since their acquisition on July 12, 2010, December 28, 2009 and March 29, 2009, respectively.

The basics segment is comprised of our business units primarily focused on garment styles that are characterized by low fashion risk, and includes our Delta Catalog and FunTees businesses. Within the Delta Catalog business, we market, distribute and manufacture unembellished knit apparel under the brands of Delta Pro Weight®, Delta Magnum Weight®, Quail Hollow®, Healthknit® and FunTees®. These products are primarily sold to screen printing and advertising specialty companies. We also manufacture private label products for major branded sportswear companies, retailers, corporate industry programs, and sports licensed apparel marketers. Typically these products are sold with value-added services such as hangtags, ticketing, hangers, and embellishment so that they are fully ready for retail. The majority of the private label products are sold through the FunTees business.

See Note 13 of the Notes to Consolidated Financial Statements for financial information regarding segment reporting, which information is incorporated herein by reference.

PRODUCTS

We specialize in the design, merchandising, sales, and marketing of a variety of casual and athletic products for men, women, juniors, youth and children at a wide range of price points through most distribution channels.

We market more specialized fashion apparel garments and headwear under our primary brands of Soffe®, The Cotton Exchange®, Intensity Athletics®, Junk Food®, and The Game® as well as other labels.

Soffe designs and markets shorts, t-shirts, performance and fleece apparel in a wide variety of colors and sizes for men, women, juniors and children. The Soffe heritage of serving the United States Military with certified physical training apparel has inspired the introduction of a new men's performance line marketed under the collection name of XT46 - Extreme Training since 1946. Our Soffe® shorts continue to enjoy a very loyal following among teenage girls, many of whom are involved in cheerleading and dance teams. Collegiate products are designed and marketed under Soffe® and The Cotton Exchange®, which has a strong reputation selling USA made collegiate apparel to college bookstores. We also provide sports team uniforms under Intensity Athletics® and performance products to support team dealers and sporting goods stores.

Junk Food is an original vintage t-shirt company and a celebrity favorite, with global distribution and rights to over 800 licensed properties. Known for its soft fabrics and amazing fits, Junk Food® has two primary product lines, its "Classics" line and a more premium "Originals" brand, along with a long standing designer collaboration with Gap Inc.

To The Game includes product offerings of innovatively designed headwear marketed primarily under The Game®, and licensed apparel under the Realtree Outfitters® and Realtree Girl® brands. To The Game is also the exclusive licensee of Salt Life® apparel, headwear, decals, bags and other accessories, selling these lifestyle brands to the outdoors and sporting goods retail markets.

Delta offers more basic, high quality apparel garments for the entire family under the Delta Pro Weight®, Delta Magnum Weight®, Quail Hollow®, Healthknit® and FunTees® brand names. Delta products are offered in a wide range of colors available in 6-month infant to adult sizes up to 4X. The Pro Weight line represents a diverse selection of mid-weight, 100% cotton silhouettes in a large color palette, including our new heathered color offerings. The Magnum Weight line is designed to give our customers a variety of silhouettes in a heavier-weight, 100% cotton fabric.

FunTees designs, markets and manufactures label custom knit t-shirts primarily to major branded sportswear companies, including Nike, Quiksilver, adidas and Columbia Sportswear. The majority of the merchandise is embellished, and we offer our customers a wide variety of packaging services so the products can be shipped store-ready.

A key to our business success is our ability anticipate and quickly respond to changing consumer preferences. We maintain a California-based design lab that provides trend reports, concepts and color trends to keep our products and designs in style. This information is used by our in-house designers and merchandisers, along with our sales and marketing personnel, who review market trends, sales results and the popularity of our latest products to design new merchandise to meet the expected future demands of our consumers.

TRADEMARKS AND LICENSE AGREEMENTS

We own several well-recognized trademarks that are important to our business. Soffe® has stood for quality and value in the athletic and activewear market for more than sixty years and Junk Food® has been known as a leading vintage t-shirt company since 1999. The Game® and Kudzu® have been registered trademarks since 1989 and 1995, respectively. Associated with The Game®, we also have registered trademarks for the Three-Bar-Design and the Circle Design, which are recognized collegiate designs. The Cotton Exchange® is also a well recognized brand in the college market. Other registered trademarks include Sweet

and Sour®, Junk Mail®, Delta®, Quail Hollow®, and Intensity Athletics®. Our trademarks are valuable assets that differentiate the marketing of our products. We vigorously protect our trademarks and other intellectual property rights against infringement.

We have distribution rights to other trademarks through license agreements. The Soffe and To The Game business units are official licensees for most major colleges and universities. Junkfood has the right to distribute trademarked apparel across athletics (including NFL), entertainment, foods, and other pop culture categories. We also have license agreements for motorsports properties (including NASCAR), Churchill Downs, golf and other various resort properties. Our license agreements are typically non-exclusive in nature and have terms that range from one to three years. In addition, in fiscal year 2010 we became the exclusive licensee for most apparel categories within the Realtree Outfitters® and Realtree Girl® outdoor lifestyle apparel brands. We expanded our lifestyle brand apparel line in fiscal year 2011 by becoming the exclusive licensee for Salt Life® apparel, headwear, decals, bags and other accessories. While historically we have been able to renew our license agreements, the loss of certain license agreements could have a material adverse effect on our results of operations. Although we are not dependent on any single license, our license agreements collectively are of significant value to our branded segment.

MARKETING

Our sales and marketing consists of both employed and independent sales representatives located throughout the country. In the branded segment, sales teams service specialty and boutique, upscale and traditional department stores, sporting goods, outdoor, military, and college bookstore customer bases. We also have a growing international presence with our Junk Food® products in Canada, Europe, Asia and Australia. In the basics segment, our sales personnel sell our knit apparel products primarily direct to large and small screen printers and into the promotional products markets. Our private label products are sold primarily to major branded sportswear companies.

During fiscal year 2011, we shipped to approximately 15,000 customers, many of whom have numerous retail doors. No single customer accounted for more than 10% of sales in fiscal years 2011, 2010 or 2009, and our strategy is to not become dependent on any single customer. Revenues attributable to foreign countries represented approximately 1% of our total consolidated net sales in each of fiscal years 2011, 2010 and 2009.

The majority of our apparel products are produced based on forecasts to permit quick shipments to our customers. Private label programs are generally made only to order or based on a customer's forecast. Our headwear products are primarily sourced based on customer orders; however, we carry certain styles in inventory to support quick-turn shipments. We aggressively explore new ways to leverage our strengths and efficiencies to meet the quick turn needs of our customers.

We have distribution facilities strategically located throughout the United States that carry in-stock inventory for shipment to customers, with most shipments made via third party carriers. In order to better serve customers, we allow products to be ordered by the piece, dozen, or full case quantities. Because a significant portion of our business consists of at-once EDI and direct catalog orders, we believe that backlog order levels do not give a general indication of future sales.

COMPETITION

We have numerous competitors with respect to the sale of apparel and headwear products in domestic and international markets, with many having greater financial resources than we do.

We believe that competition within our branded segment is based primarily upon design, brand recognition, and consumer preference. We focus on sustaining the strong reputation of our brands by adapting our product offerings to changes in fashion trends and consumer preferences. We keep our merchandise fresh with unique artwork and new designs, and support the integrated lifestyle statement through effective consumer marketing. We believe that our favorable competitive position includes strong consumer recognition and brand loyalty, the high quality of our products, and our flexibility and process control, which help lead to product consistency. Our ability to remain competitive in the areas of quality, price, design, marketing, product development, manufacturing, technology and distribution will, in large part, determine our future success.

Competition in our undecorated basics business is generally based upon price, service, delivery time and quality, with the relative importance of each factor depending upon the needs of the particular customers and the specific product offering. As this business is highly price competitive, competitor actions can greatly influence pricing and demand for our products. While price is still important in the private label market, quality and service are more important factors for customer choice. Our ability to consistently service the needs of our private label customers greatly impacts the future business with these customers.

SEASONALITY

Although our various product lines are sold on a year-round basis, the demand for specific products or styles reflects some seasonality, with sales in our fourth fiscal quarter generally being the highest and sales in our second fiscal quarter generally being the lowest. The percentage of net sales by quarter for the year ended July 2, 2011 was 23%, 22%, 26% and 29% for the first, second, third, and fourth fiscal quarters, respectively. Consumer demand for apparel is largely influenced by the overall U.S.

economy and consumer spending in general. Therefore, the distribution of sales by quarter in fiscal year 2011 may not be indicative of the distribution in future years.

MANUFACTURING

We have a vertically integrated manufacturing platform that supports both our branded and basics segment. Our manufacturing operations begin with the purchase of yarn and other raw materials from third-party suppliers. We manufacture fabrics in either our company-owned domestic textile facility located in Maiden, North Carolina or in Ceiba Textiles, our leased textile facility located near San Pedro Sula, Honduras. In addition, we may purchase fabric from third party contractors to supplement our internal production. The manufacturing process continues at one of our seven apparel manufacturing facilities where the products are ultimately sewn into finished garments. These facilities are either company-owned and operated, or leased and operated by us. These facilities are located domestically (two in North Carolina) and internationally (two in Honduras, one in El Salvador and two in Mexico). Our garments may also be embellished and prepared for retail (with any combination of services, including ticketing, hang tags, and hangers). In fiscal years 2011, 2010 and 2009 approximately 69%, 74% and 76%, respectively, of our manufactured products were sewn in company-operated locations. The remaining products were sewn by outside contractors located primarily in the Caribbean basin.

At the 2011, 2010 and 2009 fiscal year-ends, our long-lived assets in Honduras, El Salvador and Mexico collectively comprised approximately 45%, 49% and 51%, respectively, of our total net property, plant and equipment, with our long-lived assets in Honduras comprising 37%, 43% and 45%, respectively. For a description of risks associated with our operations located outside the United States, see Item 1A. Risk Factors.

Along with our internal manufacturing, we purchase fabric, undecorated products and full-package products from independent sources throughout the world. In fiscal years 2011, 2010 and 2009, we sourced approximately 23%, 25% and 11%, respectively, of our products from third parties. We expanded our product line into headwear in the fourth quarter of fiscal year 2009 with the acquisition of To The Game. Because our headwear merchandise is all sourced from third parties, the addition of this product line drove the increase in sourced products in fiscal year 2010.

RAW MATERIALS

We have a supply agreement with Parkdale America, LLC (“Parkdale”) to supply our yarn requirements until December 31, 2011. Under the supply agreement, we purchase from Parkdale all of our yarn requirements for use in our manufacturing operations, excluding yarns that Parkdale does not manufacture or cannot manufacture due to temporary capacity constraints. The purchase price of yarn is based upon the cost of cotton plus a fixed conversion cost. We are currently in negotiations to secure a new agreement to supply our yarn requirements. We do not believe we will lose any competitive position we currently have with a new agreement. If Parkdale’s operations are disrupted and it is not able to provide us with our yarn requirements, we may need to obtain yarn from alternative sources. Although alternative sources are presently available, we may not be able to enter into short-term arrangements with substitute suppliers on terms as favorable as our current terms with Parkdale. Because there can be no assurance that we would be able to pass along our higher cost of yarn to our customers, this could have a material adverse effect on our results of operations.

We also purchase specialized fabrics that we currently do not have the capacity or capability to produce and may purchase other fabrics when it is cost-effective to do so. While these fabrics typically are available from various suppliers, there are times when certain yarns become limited in quantity, causing some fabrics to be difficult to source. This can result in higher prices or our inability to provide products to our customers which could negatively impact our results of operations. Our dyes and chemicals are also purchased from several suppliers. While historically we have not had difficulty obtaining sufficient quantities of dyes and chemicals for our manufacturing, the availability of products can change, which could require us to adjust dye and chemical formulations. In certain instances, these adjustments can increase our manufacturing costs, negatively impacting our results of operations.

EMPLOYEES AND SOCIAL RESPONSIBILITY

As of July 2, 2011, we employed approximately 7,200 full time employees, of whom approximately 1,800 were employed in the United States. There are approximately 1,000 employees in Honduras that are covered by a collective bargaining agreement. We have never had a strike or legal work stoppage, and believe that our relations with our employees are good. We have invested significant time and resources in ensuring that the working conditions in all of our facilities meet or exceed the standards imposed by the governing laws. We have obtained WRAP (Worldwide Responsible Accredited Production) certification for all of our manufacturing facilities that we operate in the United States, Honduras, El Salvador and Mexico. Soffe and To The Game are affiliates of FLA (Fair Labor Association) as college licensees. In 2011, Delta Apparel, Inc. applied for and was approved by the FLA board as a provisional participating company. This level of affiliation with FLA will further enhance human rights compliance monitoring for Delta Apparel plants and our third party contractors. In addition, we have proactive programs to promote workplace safety, personal health, and employee wellness. We also support educational institutions in the communities where we operate.

ENVIRONMENTAL AND REGULATORY MATTERS

We are subject to various federal, state and local environmental laws and regulations concerning, among other things, wastewater discharges, storm water flows, air emissions and solid waste disposal. Our plants generate very small quantities of hazardous waste, which are either recycled or disposed of off-site. Most of our plants are required to possess one or more permits, and we believe that we are currently in compliance with the requirements of these permits.

The environmental rules applicable to our business are becoming increasingly stringent. We incur capital and other expenditures annually to achieve compliance with environmental standards, and currently do not expect the amount of expenditures required to comply with the environmental laws will have a material adverse effect on our operations, financial condition or liquidity. There can be no assurance, however, that future changes in federal, state, or local regulations, interpretations of existing regulations or the discovery of currently unknown problems or conditions will not require substantial additional expenditures. Similarly, while we are not currently aware of any violations, the extent of our liability, if any, for past failures to comply with laws, regulations and permits applicable to our operations cannot be determined and could have a material adverse effect on our operations, financial condition or liquidity.

AVAILABLE INFORMATION

Our corporate internet address is www.deltaapparelinc.com. We make available free of charge on our website our SEC reports, including our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Section 16 filings and any amendments to those reports, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information found on our website is not part of this, or any other, report that we file with or furnish to the SEC.

In addition, we will provide upon request, at no cost, paper or electronic copies of our reports and other filings made with the SEC. Requests should be directed to: Investor Relations Department, Delta Apparel, Inc., 322 South Main Street, Greenville, South Carolina 29601. Requests can also be made by telephone to 864-232-5200 extension 6621, or via email at investor.relations@deltaapparel.com.

We operate in a rapidly changing, highly competitive business environment that involves substantial risks and uncertainties, including, but not limited to, the risks identified below. The following factors, as well as factors described elsewhere in this report or in our other filings with the SEC, which could materially affect our business, financial condition or operating results, should be carefully considered in evaluating our Company and the forward-looking statements contained in this report or future reports. The risks described below are not the only risks facing our Company. Additional risks not presently known to us or that we currently do not view as material, may become material, and may impair our business operations. Any of these risks could cause, or contribute to causing, our actual results to differ materially from expectations.

The price of purchased yarn and other raw materials is prone to significant fluctuations and volatility. Cotton is the primary raw material used in the manufacture of our apparel products. The price of cotton fluctuates and is affected by weather, consumer demand, speculation on the commodities market, and other factors that are generally unpredictable and beyond our control. As described under the heading “Raw Materials”, the price of yarn purchased from Parkdale is based upon the cost of cotton plus a fixed conversion cost. We set future cotton prices with purchase commitments as a component of the purchase price of yarn in advance of the shipment of finished yarn from Parkdale. Prices are set according to prevailing prices, as reported by the New York Cotton Exchange, at the time we enter into the commitments. Thus, we are subject to the commodity risk of cotton prices and cotton price movements, which could result in unfavorable yarn pricing for us. For example, we estimate that a change of $0.01 per pound in cotton prices would affect our annual raw material costs by approximately $6.9 million at current levels of production. The ultimate effect of this change on our earnings cannot be quantified, as the effect of movements in cotton prices on industry selling prices are uncertain. Cotton prices surged upward during 2010 and early 2011, but have recently declined significantly from the high. The ultimate impact on selling prices from the decline is not yet known, but may require us to reduce selling prices in response to competitive pricing pressure, which could adversely impact our results of operations in the short-term. We will be bringing in yarn with the highest cotton cost in our first quarter of fiscal year 2012, and expect the cotton cost to decline over the remaining quarters. As this yarn flows through our manufacturing process and the finished goods are sold, we expect the highest cost inventory will be in our cost of sales during our second and third quarters of fiscal year 2012, impacting gross margins most significantly in these quarters. In addition, if Parkdale’s operations are disrupted and it is not able to provide us with our yarn requirements, we may need to obtain yarn from alternative sources. We may not be able to enter into short-term arrangements with substitute suppliers on terms as favorable as our current terms with Parkdale, which could negatively affect our business.

Current economic conditions may adversely impact demand for our products. The apparel industry is cyclical and dependent upon the overall level of discretionary consumer spending which changes as regional, domestic and international economic conditions change. These economic conditions include, but are not limited to, employment levels, energy costs, interest rates, tax rates, inflation, personal debt levels, and uncertainty about the future with many of these factors outside of our control. Overall,

consumer purchases of discretionary items tend to decline during recessionary periods when disposable income is lower. As such, further deterioration in general economic conditions that creates uncertainty or alters discretionary consumer spending habits could reduce our sales. Because we match our manufacturing production to demand, weakening sales may require us to reduce output, thereby increasing per unit costs and lowering our gross margins, causing a material adverse effect on our results of operations.

Deterioration of the financial condition of our customers could adversely affect our financial position and results of operations. We extend credit to our customers, generally without requiring collateral. The extension of credit involves considerable judgment and is based on an evaluation of each customer’s financial condition and payment history. We monitor our credit risk exposure by periodically obtaining credit reports and updated financial statements on our customers. Further deterioration in the economy, continued decline in consumer purchases of apparel, or further disruption in the ability of our customers to access liquidity could have an adverse effect on the financial condition of our customers. During the past several years, various retailers and other customers have experienced significant difficulties, including restructurings, bankruptcies and liquidations. The inability of these retailers and other customers to overcome these difficulties may increase due to the current worldwide economic conditions. We maintain an allowance for doubtful accounts for potential credit losses based upon current conditions, our historical trends and other available information. However, the inability to collect on sales to significant customers or a group of customers could have a material adverse effect on our financial condition and results of operations.

The apparel industry is highly competitive, and we face significant competitive threats to our business. The market for athletic and activewear apparel and headwear is highly competitive and includes new competitors as well as increased competition from established companies, some of which are larger, more diversified, and may have greater financial resources than we do. Many of our competitors have competitive advantages, including larger sales forces, better brand recognition among consumers, larger advertising budgets, and greater economies of scale. If we are unable to compete successfully with our competitors, our business and results of operations will be adversely affected.

We currently pay income taxes at lower than statutory rates. We are subject to income tax in the United States and in foreign jurisdictions in which we generate net operating profits. We benefit from a lower overall effective income tax rate due to the majority of our manufacturing operations being located in foreign tax-free locations. Our U.S. legal entity contracts with our foreign subsidiaries to manufacture products on its behalf with the intercompany prices paid for the manufacturing services and manufactured products based on an arms-length standard and supported by an economic study. We have concluded that the profits earned in the tax-free locations will be considered permanently reinvested. Thus, no U.S. deferred tax liability is recorded on these profits, causing our effective tax rate to be significantly below U.S. statutory rates. Our effective tax rate could be adversely affected by changes in the mix of earnings between the U.S. and tax-free foreign jurisdictions. In addition, changes to U.S. tax laws impacting how U.S. multinational corporations are taxed on foreign earnings, a need or requirement for us to remit tax-free earnings back to the U.S., could also have a material adverse effect on our tax expense and cash flow.

We may be restricted in our ability to borrow under our revolving credit facility. Significant operating losses or significant uses of cash in our operations could cause us to default on our asset-based revolving credit facility. Our ability to borrow under the credit facility depends on our accounts receivable and inventory levels. A significant deterioration in our accounts receivable or inventory levels could restrict our ability to borrow funds. In addition, our credit facility includes a financial covenant that if the amount of availability falls below an amount equal to 12.5% of the lesser of the borrowing base or $145 million, our Fixed Charge Coverage Ratio (“FCCR”) (as defined in our credit agreement) for the preceding 12 month period must not be less than 1.1 to 1.0. In addition, the credit facility includes customary conditions to funding, representations and warranties, covenants, and events of default. The covenants include, among other things, limitations on asset sales, consolidations, mergers, liens, indebtedness, loans, investments, guaranties, acquisitions, dividends, stock repurchases, and transactions with affiliates. An event of default under the credit facility could result in an acceleration of our obligations under the agreement, in the foreclosure on any assets subject to liens in favor of the credit facility’s lenders, and in our inability to borrow additional amounts under the credit facility. Although our availability at July 2, 2011, was $59.1 million and our FCCR for the preceding twelve months was 3.8x, a significant decline in our profitability could cause our FCCR to fall below 1.1x, thereby requiring us to maintain a minimum availability as defined in our credit agreement. This could restrict our ability to borrow funds and adversely affect our financial position and results of operations.

We may need to raise additional capital to grow our business through acquisitions. While our existing credit facility should be adequate to support our existing business in the foreseeable future, the rate of our growth, especially through acquisitions, will depend on the availability of debt and equity capital. We may not be able to raise capital on terms acceptable to us or at all. If new sources of financing are required, but are insufficient or unavailable, we may be required to modify our growth and operating plans based on available funding, which could adversely affect our ability to grow the business.

We have expanded our business through acquisitions that could result in diversion of resources, an inability to integrate acquired operations and extra expenses. Our growth strategy involves acquiring businesses that complement of our existing business. The negotiation of potential acquisitions and integration of acquired businesses could divert our management’s attention from our existing businesses which could negatively impact the results of operations. In addition, if the integration of an acquired business is not successful or takes significantly longer than expected, or if we are unable to realize the expected benefits from an

acquired business, it could adversely affect our financial condition and results of operations.

The price of energy and fuel costs are prone to significant fluctuations and volatility which could adversely affect our results of operations. Our manufacturing operations require high inputs of energy, and therefore changes in energy prices directly impact our gross profits. In addition, we incur significant freight costs to transport goods between the United States and our offshore facilities, along with transportation expenses to ship products to our customers. The cost of energy and fuel fluctuate due to a number of factors outside our control, including government policy and regulation and weather conditions. We continue to focus on manufacturing methods that will reduce the amount of energy used in the production of our products to mitigate risks of fluctuations in the cost of energy. In addition, we enter into forward contracts to fix a portion of our expected natural gas requirements for delivery in the future in order to mitigate potential increases in costs. However, significant increases in energy and fuel prices may make us less competitive compared to others in the industry, which may have a material adverse effect on our results of operations.

Our business operations rely on our information systems and any material disruption or slowdown of our systems could cause operational delays. We depend on information systems to manage our inventory, process transactions, respond to customer inquiries, purchase, sell and ship goods on a timely basis and maintain cost-effective operations. We have invested significant capital and expect future capital expenditures associated with the integration of our information technology systems across our businesses. This process involves the replacement and consolidation of technology platforms so our businesses are served by fewer platforms, resulting in operational efficiencies and reduced costs. Our inability to effectively convert our operations to the new systems could cause delays in product fulfillment and reduced efficiency in our operations. In addition, we may experience operational problems with our information systems as a result of system failures, viruses, security breaches, disasters or other causes. Any material disruption or slowdown of our information systems could cause operational delays that could have a material adverse effect on our results of operations.

Our business could be harmed if we are unable to deliver our products to the market due to problems with our distribution network. We have company-owned and leased distribution facilities located throughout the United States. Any significant interruption in the operation of any of these facilities, whether within or outside of our control, may delay shipment of merchandise to our customers, potentially damaging our reputation and causing a loss of revenue. In addition, if we are unable to successfully coordinate the planning of inventory across these facilities and the distribution activities, it could have a material adverse effect on our financial condition and results of operations.

Failure of our operations to comply with environmental regulation could have a material adverse effect on our financial position and results of operations. Our operations must meet extensive federal, state and local regulatory standards in the areas of safety, health and environmental pollution controls. There can be no assurance that interpretations of existing regulations, future changes in existing laws, or the enactment of new laws and regulations will not require substantial additional expenditures. Although we believe that we are in compliance in all material respects with existing regulatory requirements, the extent of our liability, if any, for the discovery of currently unknown problems or conditions, or past failures to comply with laws, regulations and permits applicable to our operations, cannot be determined and could have a material adverse effect on our financial position and results of operations.

We are subject to periodic litigation in both domestic and international jurisdictions that may adversely affect our financial position and results of operations. From time to time we may be involved in legal actions regarding product liability, employment practices, trademark infringement, bankruptcies and other litigation. Due to the inherent uncertainties of litigation in both domestic and foreign jurisdictions, we cannot accurately predict the ultimate outcome of any such proceedings. Proceedings could cause us to incur costs and may require us to devote resources to defend against these claims and could ultimately result in a loss against these claims, which could adversely affect our financial position and results of operations. For a description of current legal proceedings, see Part I, Item 3, Legal Proceedings.

Our success depends, in part, on our ability to predict or effectively react to changing consumer preferences and trends. The success of our businesses depends on our ability to anticipate and respond quickly to changing consumer demand and preferences in apparel and headwear. We believe that our brands are recognized by consumers across many demographics. The popularity, supply and demand for particular products can change significantly from year to year based on prevailing fashion trends and other factors and therefore our ability to adapt to fashion trends in designing our products is important to the success of our brands. If we are unable to quickly adapt to changes in consumer preferences in the design of our products, our results of operations could be adversely affected.

We rely on the strength of our trademarks and could incur significant costs to protect these trademarks. Our trademarks, including Soffe®, Junk Food®, The Game®, and The Cotton Exchange® among others, are important to our marketing efforts and have substantial value. In addition, we have trademarked the Three-Bar-Design and the Circle Design, which are recognized collegiate designs. We aggressively protect these trademarks and have incurred legal costs in the past to establish and protect these trademarks, but these costs have not been significant. We may in the future be required to expend additional resources to protect these trademarks. The loss or limitation of the exclusive right to use our trademarks could adversely affect our sales and

results of operations.

A significant portion of our business relies upon license agreements. We rely on licensed products for a significant part of our sales. Although we are not dependent on any single license, we believe that our license agreements in the aggregate are of significant value to our business. The loss of or failure to obtain license agreements could adversely affect our sales and results of operations.

We may be subject to the impairment of acquired intangible assets. When we acquire a business, a portion of the purchase price of the acquisition may be allocated to goodwill and other identifiable intangible assets. The amount of the purchase price that is allocated to goodwill and other intangible assets is determined by the excess of the purchase price over the net identifiable assets acquired. At July 2, 2011 and July 3, 2010, our goodwill and other intangible assets were approximately $24.2 million and $25.4 million, respectively. We conduct an annual review, and more frequent reviews if events or circumstances dictate, to determine whether goodwill is impaired. We also determine whether impairment indicators are present related to our identifiable intangible assets. If we determine that goodwill or intangible assets are impaired, we would be required to write down the value of these assets. Based upon the operating results and projections for Art Gun, during our second fiscal quarter we concluded that the goodwill and contingent consideration associated with the Art Gun acquisition were impaired. The change in contingent consideration (a $1.5 million favorable adjustment) and full impairment of the Art Gun goodwill (a $0.6 million impairment charge) resulted in a net favorable adjustment of $0.9 million, which was recorded in our second fiscal quarter and is included in the branded segment (See Note 2(m) to our Consolidated Financial Statements). We completed our annual impairment test of goodwill on the first day of our third fiscal quarter using actual results through the last day of the second fiscal quarter. Based on the valuation, there does not appear to be impairment on the goodwill associated with Junkfood, the only remaining goodwill recorded on our financial statements. We also concluded that there are no additional indicators of impairment related to our intangible assets. There can, however, be no assurance that we will not be required to take an impairment charge in the future, which could have a material adverse effect on our results of operations.

Changes in the regulations and laws regarding e-commerce could reduce the growth and lower the profitability of our internet sales. The e-commerce industry has undergone, and continues to undergo, rapid development and change. There have been continuing efforts to increase the legal and regulatory obligations and restrictions on companies conducting commerce through the internet, primarily in the areas of taxation, consumer privacy and protection of consumer personal information. These laws and regulations could increase the costs and liabilities associated with our e-commerce activities, thereby negatively impacting our results of operations.

Our basics segment is subject to significant pricing pressures which may decrease our gross profit margins if we are unable to implement our cost reduction strategies. We operate our basics segment in a highly competitive, price sensitive industry. Our strategy in this market environment is to be a low-cost producer and to differentiate ourselves by providing quality products and value-added services to our customers. To help achieve this goal, we began production in Ceiba Textiles, our Honduran textile facility, in fiscal year 2008. In the fourth quarter of fiscal year 2009, we closed our Soffe textile manufacturing facility in Fayetteville, North Carolina and moved this production to our Maiden, North Carolina and Ceiba Textiles plants. In fiscal year 2010, we began the expansion of Ceiba Textiles to increase internal manufacturing capacity and further leverage the fixed cost of the facility, and continued the expansion during fiscal year 2011. These initiatives, along with continual improvements in our production and delivery of products, are expected to lower our product costs and improve our results of operations. Failure to achieve the cost savings expected from these initiatives could have a material adverse effect on our results of operations.

Our operations are subject to political, social, economic, and climate risks in Mexico, Honduras and El Salvador. The majority of our products are manufactured in Honduras, El Salvador and Mexico, with a concentration in Honduras. These countries have experienced political, social and economic instability in the past, and we cannot be certain of their future stability. Instability in a country can lead to protests, riots and labor unrest. New government leaders can change employment laws, thereby increasing our costs to operate in that country. In addition, fire or natural disasters, such as hurricanes, earthquakes, or floods can occur in these countries. Any of these political, social, economic or climatic events or conditions could disrupt our supply chain or increase our costs, adversely affecting our financial position and results of operations.

Significant changes to international trade regulations could adversely affect our results of operations. The majority of our products are manufactured in Honduras, El Salvador and Mexico. We therefore benefit from current free trade agreements and other duty preference programs, including the North American Free Trade Agreement (“NAFTA”) and the Central America Free Trade Agreement (“CAFTA”). Our claims for duty free or reduced duty treatment under CAFTA, NAFTA and other available programs are largely conditioned on our ability to produce or obtain accurate records, some of which are provided to us by third parties, about production processes and sources of raw materials. Subsequent repeal or modification of NAFTA or CAFTA, or the inadequacy or unavailability of supporting records, could materially adversely affect our results of operations. In addition, our products are subject to foreign competition, which in the past has been faced with significant U.S. government import restrictions. The extent of import protection afforded to domestic apparel producers has been, and is likely to remain, subject to political considerations. The elimination of import protections for domestic apparel producers could significantly increase global competition, which could adversely affect our business. In addition, any failure to comply with international trade regulations could cause us to become subject to investigation resulting in significant penalties or claims or our inability to conduct our business,

adversely affecting our results of operations.

Changes in domestic or foreign employment regulations or changes in our relationship with our employees could adversely affect our results of operations. We employ approximately 7,200 employees worldwide, with approximately 5,400 of these employees being in Honduras, El Salvador or Mexico. Changes in domestic and foreign laws governing our relationships with our employees, including wage and human resources laws and regulations, fair labor standards, overtime pay, unemployment tax rates, workers' compensation rates and payroll taxes, would likely have a direct impact on our operating costs. A significant increase in wage rates in the countries in which we operate could have a material impact on our operating results. Our employees are currently not party to any collective bargaining agreements, with the exception of approximately 1,000 employees in Honduras, which are party to a three year collective bargaining agreement. We have historically operated our facilities in a productive manner without significant labor disruptions, such as strikes or work stoppages. However, if labor relations were to change, it could adversely affect the productivity and ultimate cost of our manufacturing operations.

We are subject to foreign currency exchange rate fluctuations. We manufacture the majority of our products outside of the United States, exposing us to currency exchange rate fluctuations. In addition, movements in foreign exchange rates can affect transaction costs because we source products from various countries. We may seek to mitigate our exposure to currency exchange rate fluctuations, but our efforts may not be successful. Accordingly, changes in the relative strength of the United States dollar against other currencies could adversely affect our business.

The value of our brands and sales of our products could be diminished by negative publicity resulting from violations in labor laws or unethical business practices. We are committed to ensuring that all of our manufacturing facilities comply with our strict internal Code of Conduct, local and internal laws, and the codes and principles to which we subscribe, including those of Worldwide Responsible Accredited Production (WRAP) and Fair Labor Association (FLA). In addition, we require our suppliers and independent contractors to operate their businesses in compliance with the laws and regulations that apply to them. However, we do not control these suppliers and independent contractors. A violation of our policies, labor laws or other laws by our suppliers or independent contractors could interrupt or otherwise disrupt our operations. Negative publicity regarding the production methods of any of our suppliers or independent contractors could adversely affect our reputation and sales, which could adversely affect our business.

The market price of Delta Apparel shares is affected by illiquidity of our shares, which could lead to our shares trading at prices that are significantly lower than expected. Various investment banking firms have informed us that public companies with relatively small market capitalizations have difficulty generating institutional interest, research coverage or trading volume. This illiquidity can translate into price discounts as compared to industry peers or to the shares’ inherent value. We believe that the market perceives us to have a relatively small market capitalization. This could lead to our shares trading at prices that are significantly lower than our estimate of their inherent value.

As of August 22, 2011, we had 8,388,413 shares of common stock outstanding. We believe that approximately 51% of our stock is beneficially owned by those who own more than 5% of the outstanding shares of our common stock. Included in the 51% are institutional investors that beneficially own more than 5% of the outstanding shares. These institutional investors own approximately 43% of the outstanding shares of our common stock. Sales of substantial amounts of our common stock in the public market by any of these large holders could adversely affect the market price of our common stock.

The market price of Delta Apparel shares is likely to be highly volatile as the stock market in general can be highly volatile. Fluctuations in Delta Apparel stock price may be influenced by, among other things, the general economic and market conditions, conditions or trends in our industry, changes in the market valuations of other apparel companies, announcements by us or our competitors of significant acquisitions, strategic partnerships or other strategic initiatives, and increased trading volumes. Many of these factors are beyond our control, but may cause the market price of our common stock to decline, regardless of our operating performance.

Our success depends upon the talents and continued contributions of our key management. We believe our future success depends on our ability to retain and motivate our key management, our ability to attract and integrate new members of management into our operations and the ability of all personnel to work together effectively as a team. Our continued success is dependent on our ability to retain existing, and attract additional, qualified personnel to execute our business strategy.

| |

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

Our principal executive office is located in a leased facility in Greenville, South Carolina. We own and lease properties supporting our administrative, manufacturing, distribution and direct outlet activities. Our products are manufactured through a combination of facilities that we either own, or lease and operate. As of July 2, 2011, we owned or leased twelve manufacturing facilities

(located in the United States, Honduras, El Salvador and Mexico) and ten distribution facilities (all within the United States). In addition, we operated six leased factory-direct stores and maintained three leased showrooms.

Our primary manufacturing and distribution facilities are as follows:

|

| | | | |

Location | | Utilization | | Segment |

Maiden Plant, Maiden, NC | | Knit/dye/finish/cut | | Basics and branded |

Ceiba Textiles, Honduras* | | Knit/dye/finish/cut | | Basics and branded |

Honduras Plant, San Pedro Sula, Honduras* | | Sew | | Basics and branded |

Cortes Plant, San Pedro Sula, Honduras* | | Sew | | Basics and branded |

Mexico Plant, Campeche, Mexico* | | Cut/sew | | Basics and branded |

Textiles LaPaz, La Paz, El Salvador* | | Sew/decoration | | Basics and branded |

Campeche Sportswear, Campeche, Mexico* | | Sew/decoration | | Basics and branded |

Fayetteville Plant, Fayetteville, NC | | Sew/decoration | | Branded |

Rowland Plant, Rowland, NC | | Sew | | Branded |

Cotton Exchange, Wendell, NC* | | Decoration | | Branded |

Art Gun Office, Miami, FL* | | Decoration/distribution | | Branded |

Downing Drive, Phenix City, AL* | | Decoration/distribution | | Branded |

Warehouse, Louisville, KY* | | Distribution | | Branded |

Distribution Center, Clinton, TN | | Distribution | | Basics |

Distribution Center, Santa Fe Springs, CA* | | Distribution | | Basics and branded |

Distribution Center, Miami, FL* | | Distribution | | Basics and branded |

Distribution Center, Cranbury, NJ* | | Distribution | | Basics and branded |

DC Annex, Fayetteville, NC* | | Distribution | | Branded |

Distribution Center, Lansing, MI* | | Distribution | | Branded |

Distribution Center, Wendell, NC* | | Distribution | | Branded |

|

| | |

* | | - Denotes leased location |

We believe that all of our facilities are suitable for the purposes for which they are designed and are generally adequate to allow us to remain competitive. We ran our manufacturing facilities near full capacity during fiscal year 2011 and currently expect our facilities to run near full capacity during fiscal year 2012. Substantially all of our assets are subject to liens in favor of our lenders under our U.S. asset-based secured credit facility and our Honduran loan.

At times we are party to various legal claims, actions and complaints. We believe that, as a result of legal defenses, insurance arrangements, and indemnification provisions with parties believed to be financially capable, such actions should not have a material effect on our operations, financial condition, or liquidity.

PART II

| |

ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Market Information for Common Stock: The common stock of Delta Apparel, Inc. is listed and traded on the NYSE Amex under the symbol “DLA”. As of August 22, 2011, there were approximately 1,007 record holders of our Common Stock.

The following table sets forth, for each of the periods indicated below, the high and low sales prices per share of our Common Stock as reported on the NYSE Amex.

|

| | | | | | | | | | | | | | | |

| Fiscal Year 2011 | | Fiscal Year 2010 |

| High | | Low | | High | | Low |

First Quarter | $ | 15.56 |

| | $ | 12.56 |

| | $ | 9.23 |

| | $ | 6.59 |

|

Second Quarter | 15.59 |

| | 12.00 |

| | 11.85 |

| | 7.52 |

|

Third Quarter | 14.78 |

| | 12.00 |

| | 15.93 |

| | 10.20 |

|

Fourth Quarter | 18.72 |

| | 13.89 |

| | 17.51 |

| | 13.89 |

|

Dividends: Our Board of Directors did not declare, nor were any dividends paid, during fiscal years 2011 and 2010. Subject to the provisions of any outstanding blank check preferred stock (none of which is currently outstanding), the holders of our common stock are entitled to receive whatever dividends, if any, may be declared from time to time by our Board of Directors in its discretion from funds legally available for that purpose. Under the terms of our credit agreement, we are allowed to make cash dividends if (i) as of the date of the payment and after giving effect to the payment, we have availability on that date of not less than $15 million and average availability for the 30 day period immediately preceding that date of not less than $15 million; and (ii) the aggregate amount of dividends and stock repurchases after May 27, 2011 does not exceed $19 million plus 50% of our cumulative net income (as defined in the credit agreement) from the first day of fiscal year 2012 to the date of determination. At July 2, 2011 and July 3, 2010, there was $18.7 million and $14.7 million, respectively, of retained earnings free of restrictions to make cash dividends.

We would expect that our Board of Directors would consider the advisability of instituting a dividend program in the future. Any future cash dividend payments will depend upon our earnings, financial condition, capital requirements, compliance with loan covenants and other relevant factors.

Purchases of our Own Shares of Common Stock: See Note 14 - Repurchase of Common Stock and Note 8 - Debt, in Item 15, which is incorporated herein by reference.

Securities Authorized for Issuance Under Equity Compensation Plans: The information required by Item 201(d) of Regulation S-K is set forth under “Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” of this Annual Report, which information is incorporated herein by reference.

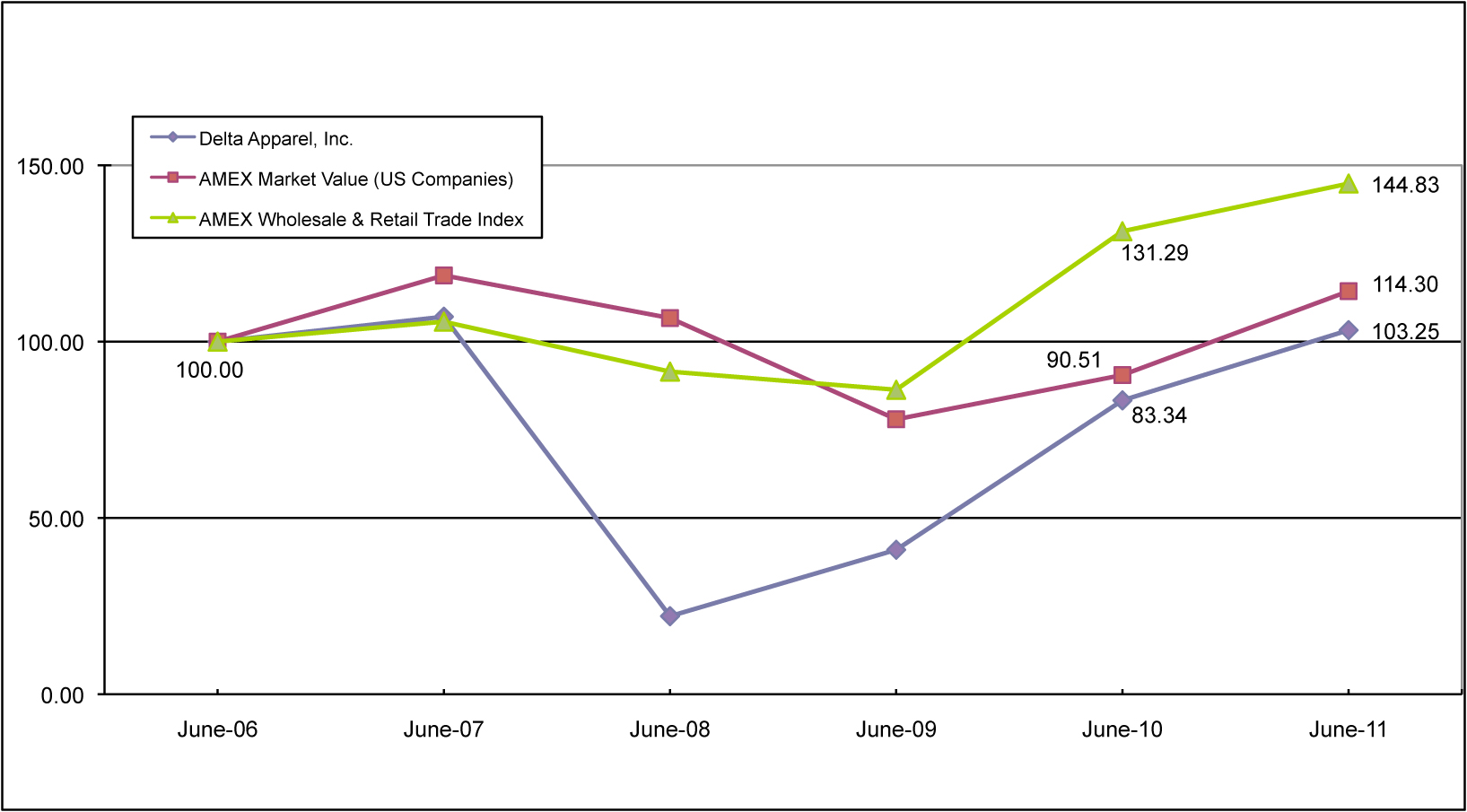

Comparison of Total Return Among Delta Apparel, Inc., NYSE Amex US Market Index, and NYSE Amex Wholesale & Retail Trade Index: Our common stock began trading on the NYSE Amex on June 30, 2000, the last trading day of our fiscal year 2000. Prior to that date, no securities of Delta Apparel were publicly traded. Set forth below is a line graph comparing the yearly change in the cumulative total stockholder return, assuming dividend reinvestment, of our common stock with (1) the NYSE Amex US Market Index (the “NYSE Amex US Market Index”) and (2) the NYSE Amex Wholesale and Retail Trade Index (the “NYSE Amex Wholesale and Retail Trade Index”), which is comprised of all NYSE Amex companies with SIC codes from 5000 through 5999. This Performance Graph assumes that $100 was invested in the common stock of our Company and comparison groups on July 1, 2006 and that all dividends have been reinvested.

|

| | | | | | | | | | | | | | | | | | | | | | | |

| 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 |

Delta Apparel, Inc. | $ | 100.00 |

| | $ | 107.06 |

| | $ | 22.12 |

| | $ | 40.95 |

| | $ | 83.34 |

| | $ | 103.25 |

|

NYSE Amex US Market Index | $ | 100.00 |

| | $ | 118.78 |

| | $ | 106.68 |

| | $ | 77.95 |

| | $ | 90.51 |

| | $ | 114.30 |

|

NYSE Amex Wholesale & Retail Trade Index | $ | 100.00 |

| | $ | 105.65 |

| | $ | 91.49 |

| | $ | 86.34 |

| | $ | 131.29 |

| | $ | 144.83 |

|

| |

ITEM 6. | SELECTED FINANCIAL DATA |

See information regarding our acquisitions within “Item 1. Business” under the heading “Acquisitions”. The selected financial data includes the financial position and results of operations of acquired businesses beginning on the date of acquisition. The consolidated statements of income for the years ended June 30, 2007 and June 28, 2008, and the consolidated balance sheet data as of June 30, 2007, June 28, 2008 and June 27, 2009 are derived from, and are qualified by reference to, our audited consolidated financial statements not included in this document. The consolidated statement of operations data for the years ended June 27, 2009, July 3, 2010 and July 2, 2011 and the consolidated balance sheet data as of July 3, 2010 and July 2, 2011 are derived from, and are qualified by reference to, our audited consolidated financial statements included elsewhere in this document. We operate on a 52-53 week fiscal year ending on the Saturday closest to June 30. All fiscal years shown were 52-week years with the exception of fiscal year 2010 which was a 53-week year. Historical results are not necessarily indicative of results to be expected in the future. The selected financial data should be read in conjunction with the Consolidated Financial Statements and the related notes as indexed on page F-1 and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7.

|

| | | | | | | | | | | | | | | | | | | |

| Fiscal Year Ended |

| July 2, 2011 |

| | July 3, 2010 |

| | June 27, 2009 |

| | June 28, 2008 |

| | June 30, 2007 |

|

| (In thousands, except per share amounts) |

Statement of Operations Data: | | | | | | | | | |

Net sales | $ | 475,236 |

| | $ | 424,411 |

| | $ | 355,197 |

| | $ | 322,034 |

| | $ | 312,438 |

|

Cost of goods sold | (359,001 | ) | | (323,628 | ) | | (278,758 | ) | | (257,319 | ) | | (239,365 | ) |

Selling, general and administrative expenses | (91,512 | ) | | (80,695 | ) | | (64,388 | ) | | (59,898 | ) | | (59,187 | ) |

Valuation adjustment, net | 918 |

| | — |

| | — |

| | — |

| | — |

|

Other (expense) income, net | (345 | ) | | 74 |

| | 96 |

| | 132 |

| | (89 | ) |

Restructuring costs * | — |

| | — |

| | — |

| | (62 | ) | | (1,498 | ) |

Operating income | 25,296 |

| | 20,162 |

| | 12,147 |

| | 4,887 |

| | 12,299 |

|

Interest expense, net | (2,616 | ) | | (3,509 | ) | | (4,718 | ) | | (6,042 | ) | | (5,157 | ) |

Income (loss) before income taxes | 22,680 |

| | 16,653 |

| | 7,429 |

| | (1,155 | ) | | 7,142 |

|

Provision (benefit) for income taxes | 5,353 |

| | 4,466 |

| | 973 |

| | (647 | ) | | 1,471 |

|

Extraordinary gain, net of taxes | — |

| | — |

| | — |

| | — |

| | 672 |

|

Net income (loss) | $ | 17,327 |

| | $ | 12,187 |

| | $ | 6,456 |

| | $ | (508 | ) | | $ | 6,343 |

|

| | | | | | | | | |

Basic earnings (loss) per common share: | | | | | | | | | |

Income (loss) before extraordinary gain | $ | 2.04 |

| | $ | 1.43 |

| | $ | 0.76 |

| | $ | (0.06 | ) | | $ | 0.67 |

|

Extraordinary gain, net of income taxes | — |

| | — |

| | — |

| | — |

| | 0.08 |

|

Net income (loss) | $ | 2.04 |

| | $ | 1.43 |

| | $ | 0.76 |

| | $ | (0.06 | ) | | $ | 0.75 |

|

| | | | | | | | | |

Diluted earnings (loss) per common share: | | | | | | | | | |

Income (loss) before extraordinary gain | $ | 1.98 |

| | $ | 1.40 |

| | $ | 0.76 |

| | $ | (0.06 | ) | | $ | 0.65 |

|

Extraordinary gain, net of income taxes | — |

| | — |

| | — |

| | — |

| | 0.08 |

|

Net income (loss) | $ | 1.98 |

| | $ | 1.40 |

| | $ | 0.76 |

| | $ | (0.06 | ) | | $ | 0.73 |

|

| | | | | | | | | |

Dividends declared per common share | $ | — |

| | $ | — |

| | $ | — |

| | $ | 0.05 |

| | 0.20 |

|

| | | | | | | | | |

Balance Sheet Data (at year end): | | | | | | | | | |

Working capital | $ | 160,646 |

| | $ | 125,163 |

| | $ | 135,369 |

| | $ | 133,917 |

| | $ | 120,645 |

|

Total assets | 311,865 |

| | 251,333 |

| | 256,993 |

| | 261,623 |

| | 232,790 |

|

Total long-term debt, less current maturities | 83,974 |

| | 62,355 |

| | 85,936 |

| | 95,542 |

| | 70,491 |

|

Shareholders’ equity | 141,965 |

| | 125,714 |

| | 112,145 |

| | 104,893 |

| | 103,669 |

|

* On July 18, 2007, we announced plans to restructure our textile manufacturing operations. The restructuring plan included the closing of our manufacturing facility in Fayette, Alabama, the expensing of excess costs associated with the integration of FunTees and the start-up expenses related to the opening of our Honduran textile facility, Ceiba Textiles.

The restructuring plan began in the fourth quarter of fiscal year 2007 and was completed in the third quarter of fiscal year 2008. In total, we incurred $11.8 million, or approximately $0.90 earnings per diluted share, in charges associated with the restructuring. During fiscal year 2007, we incurred a total of $6.9 million, or $0.51 per diluted share, of which $5.4 million was recorded in cost of sales and $1.5 million on the restructuring cost line item of the financial statements. During fiscal year 2008, we incurred $4.9 million, or $0.39 per diluted share, in charges associated with the restructuring plan, of which $4.8 million was included in cost of sales with the remaining $0.1 million on the restructuring cost line item of the financial statements. All charges associated with the restructuring plan were recorded in our basics segment.

| |

ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

BUSINESS OUTLOOK

While we are encouraged with the results we achieved in fiscal year 2011 and with our long term prospects, the continued weakness in the global economy and extreme volatility in input costs are presenting unique obstacles. In fiscal year 2012 we will need to manage through the higher cost cotton rolling through cost of sales, impacting our second and third fiscal quarters most significantly.

Over the last several years we have continued to improve the performance of our manufacturing operations which we believe has improved our competitive position. Our continuous improvement and six sigma programs continued to lower product cost by improving yields, reducing waste and minimizing off quality production. In fiscal year 2011 we expanded the output in most of our manufacturing facilities which leverages our fixed costs and provides additional volume to sell. We ran our manufacturing at capacity during fiscal year 2011 and currently expect to continue this into fiscal year 2012, taking advantage of the capacity expansions we completed over the past twelve months.

Our customer base for private label and decorated products is expanding and should add revenue in our basics segment for the upcoming year. Market demand for our private label programs remains strong, driven by consumer demand for our customers' products and the high service levels required in this marketplace. Demand for undecorated tees has recently weakened causing additional challenges in the catalog tee business.

We expect our branded segment to continue its growth trends in the upcoming year with improved operating margins. Our Soffe business continues to gain new doors, particularly with the sporting goods distribution channel. During fiscal year 2011 we completed most of the integration work on The Cotton Exchange and expect to see the benefits of this in fiscal year 2012. We are seeing positive trends in our Junkfood business and expect sales growth in fiscal year 2012, driven by solid business with The Gap, along with improved results with boutiques and upper tier retailers. Junkfood has been focused on brand building, resulting in strong press coverage over the past six months.